Quick Summary

Underwriting automation with AI agents is changing the way risks are evaluated by insurers and lenders. This blog outlines how AI agents will revolutionize the underwriting process in terms of efficiency, fraud detection, compliance, and decision-making for insurance, loans, and mortgages. Using underwriting automation through AI agents, organizations can achieve efficiency and effectiveness in their underwriting processes.

Key Takeaways

- Automate document collection and verification

- Improve risk scoring with real-time data

- Identify fraud faster across multiple sources

- Minimize underwriting processing times

- Improve compliance and auditability

- Improve borrower and policyholder experience

- Expand underwriting without increasing workforce

What happens when an underwriting process, which was built to be manual, paper-based, and time-consuming, adapts to meet rising customer demands, regulatory requirements, and faster processing times? For many years, the process of underwriting was executed by manually examining documentation, verifying facts, assessing risks, and making decisions for each individual document. It may have worked in the past, but it caused delays, irregularities, and high costs.

With underwriting AI agents, all these processes can be automated. Not only do such AI agents learn through machine learning, but they also combine all aspects of the process of underwriting into a connected system. By 2028, 33% of enterprise software applications are expected to include agentic AI, up from less than 1% in 2024. At the same time, 77% of insurance executives say they need to adopt generative AI quickly to keep up with competitors.

What Is Underwriting Automation? (Definition & Evolution)

Underwriting is the process of evaluating risk. Whether a lender is deciding whether to approve a mortgage, an insurer is pricing a commercial liability policy, or a bank is analyzing a business loan, the fundamental question is the same that what is the probability that this goes wrong, and how much should we charge for taking that risk? For most of the industry's history, answering that question required a human being to sit down with a file, review dozens of documents, cross-reference data from multiple sources, and apply judgment built from years of experience. It worked, but it significantly cost time, accuracy, and consistency.

The underwriting automation began with rules engines in the 1990s that analyzed straightforward applications based on criteria set beforehand. The problem with such systems was that they worked quickly on straightforward applications but were fragile when the applications shifted from standard protocols. The next wave brought machine learning and predictive analysis that helped build models to accurately analyze credit risk while spotting any red flags that might otherwise escape human detection. Despite these advancements, automation acted only as an assistive tool, with final decision-making consistently resting with human operators. The game changer has been agentive intelligence, algorithms that not only score the applications and spot red flags but also direct the whole underwriting process.

Traditional vs AI-Powered Underwriting

Traditional underwriting is sequential and entirely human-dependent. An underwriter receives a submission, manually gathers documents from multiple sources, verifies data by hand, applies risk scoring, checks compliance, and then issues a decision, with each step waiting on the previous one. According to some reports, more than a third of an underwriter's time is still spent on non-core tasks like data collection and administrative work. When a document is missing or a reviewer is overloaded, the file simply sits idle.

| Factor | Traditional Underwriting | AI-Powered Underwriting |

|---|---|---|

| Process Flow | Sequential, step-by-step | Parallel, multi-agent simultaneously |

| Decision Time | Days to weeks | Minutes to hours |

| Risk Assessment | Static, point-in-time snapshot | Dynamic, continuously updated |

| Consistency | Varies by individual and workload | Same logic applied every time |

| Compliance | Separate downstream review | Built into the workflow in real time |

| Cost per File | High, labour-intensive | Up to 50% lower operational cost |

AI-powered underwriting flips the traditional underwriting approach. Several agents work simultaneously to extract documents, score risks, detect fraud, and perform regulatory checks. The outcome is not only speed, but also increased reliability and scalability, where the quality is never compromised by deadlines, and underwriters can focus on the tasks that require their attention.

Curious how much faster your underwriting process could be with AI agents?

Talk to our expertsWhat Are AI Agents for Underwriting? (Agentic AI Explained)

AI agents are neither chatbots nor workflow rules. The AI agents are systems that have the ability to observe their environments, take decisions based on such perceptions, act upon these decisions, and learn from these actions. This becomes evident in the case of underwriting through the concept of multi-agent architecture. Here, a master orchestrator controls the whole process while the specialized underwriting AI agents perform specialized tasks such as extracting and validating the documents, evaluating the credit risk, analyzing the fraudulent behaviour of the client, and ensuring compliance with laws.

The difference between the underwriting ai agents process and the traditional automation process lies in the fact that AI agents can process unstructured data. They read broker submissions written in natural language, extract relevant fields, cross-check them against internal and external databases, and flag irregularities without human direction at each step.

How does AI transform the underwriting process?

The transformation happens across the full workflow, not just at a particular decision point.

Intake Automation

Agents works on unstructured submissions like PDFs, emails, and broker documents to extract all related fields, identify gaps, and automatically request missing information. What once used to take hours of manual classification now takes just minutes.

Risk Intelligence

Machine Learning models evaluate hundreds of data points in parallel, including signals like satellite imagery for property conditions, usage-based driving data for auto risk, and payment behavior patterns for credit assessment and data points most human operators would never access.

Compliance Integration

Regulatory requirements are applied during the normal workflow process as all actions are tracked for transparency, unlike the traditional model, where it’s done in a follow-up manner.

Decision Routing

The automated process auto-approves clear cases while routing borderline cases to underwriters with all the relevant data already available to them.

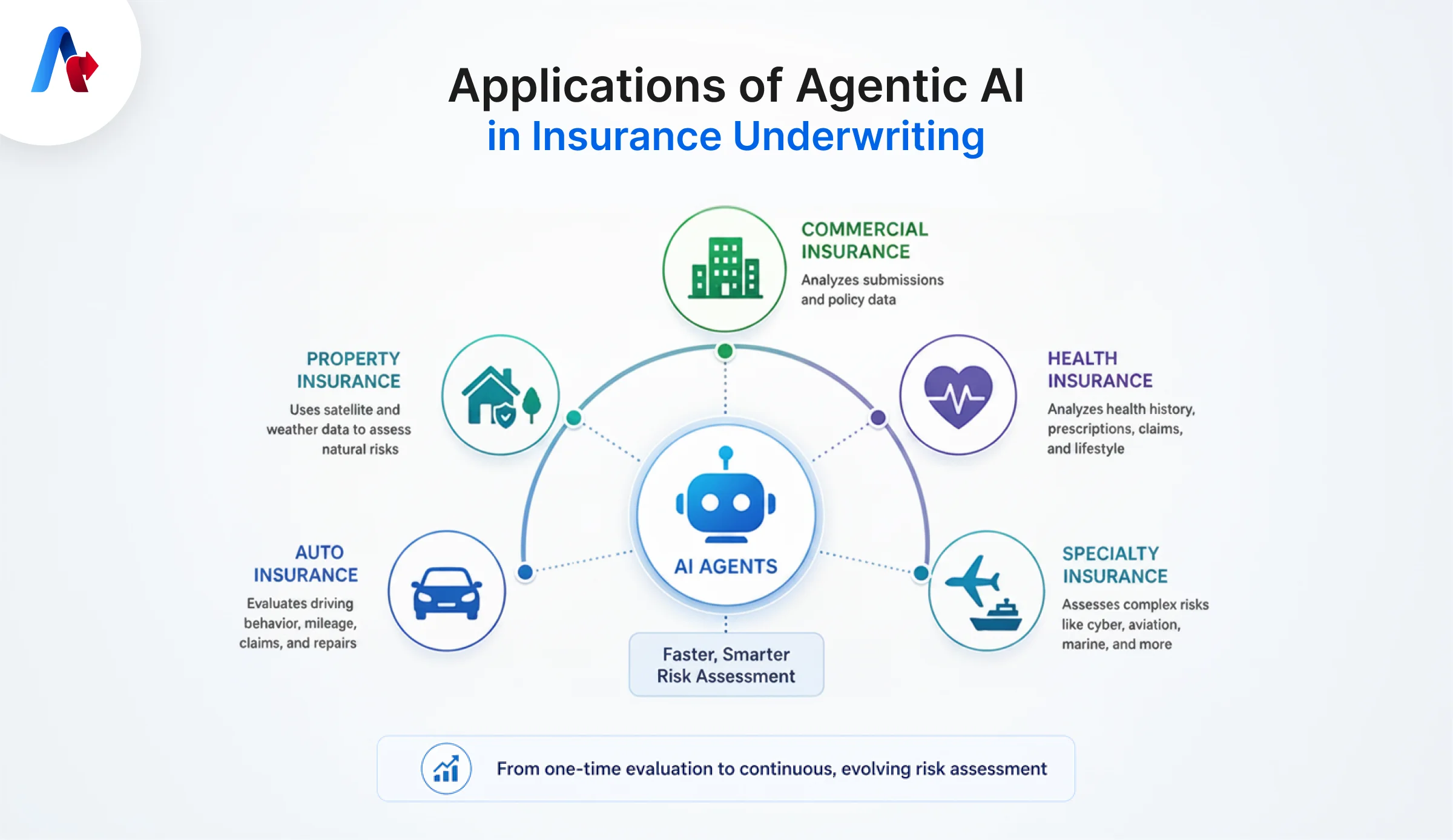

Applications of Agentic AI in Insurance Underwriting

Agentic AI in insurance underwriting is being used across commercial, property, health, auto, and specialty insurance. Instead of relying only on static risk models and manual reviews, insurers are using underwriting AI agents to evaluate information faster and more accurately.

- Commercial Insurance - Underwriting AI agents can examine the broker submissions, analyze policy information, compare the risk factors to company policies, and highlight missing information before the document is examined by a human underwriter.

- Property Insurance - The AI agents will use satellite images and weather data to evaluate the risks of wildfires, flooding, and storms.

- Auto Insurance - Underwriting automation will allow the company to consider information such as mileage, driving behavior, claims, and repair information when developing their pricing model.

- Health Insurance - The AI agents will be able to analyze patient history, prescriptions, claims behavior, and even lifestyle for patients that have higher risk factors.

- Specialty Insurance - Insurers in the cyber, aviation, marine, and professional liability sectors can use AI to evaluate more information.

The larger trend is that insurers are moving away from one-time risk evaluation and toward evolving risk analysis that changes as new information becomes available.

Key Features of the Best Underwriting AI Agents

The best underwriting AI agents combine automation, intelligence, transparency, and compliance.

- Document Intelligence - One of the most important features of underwriting AI agents is the ability to read PDFs, scanned forms, emails, broker submissions, and financial statements.

- Real-Time Scoring - Instead of depending only on past data, underwriting AI agents continuously update risk profiles as new information becomes available.

- Fraud Detection - AI agents will be able to verify details across the claim history, payment history, identities, and third-party sources to identify any irregularities.

- Compliance Monitoring - The best underwriting automation platforms will automatically follow the regulatory guidelines and keep an audit record of all processes.

- Transparency - Strong underwriting AI agents will be able to explain their reasoning process for approving, declining, or referring an application.

AI Agents for Loan Underwriting: Use Cases & Benefits

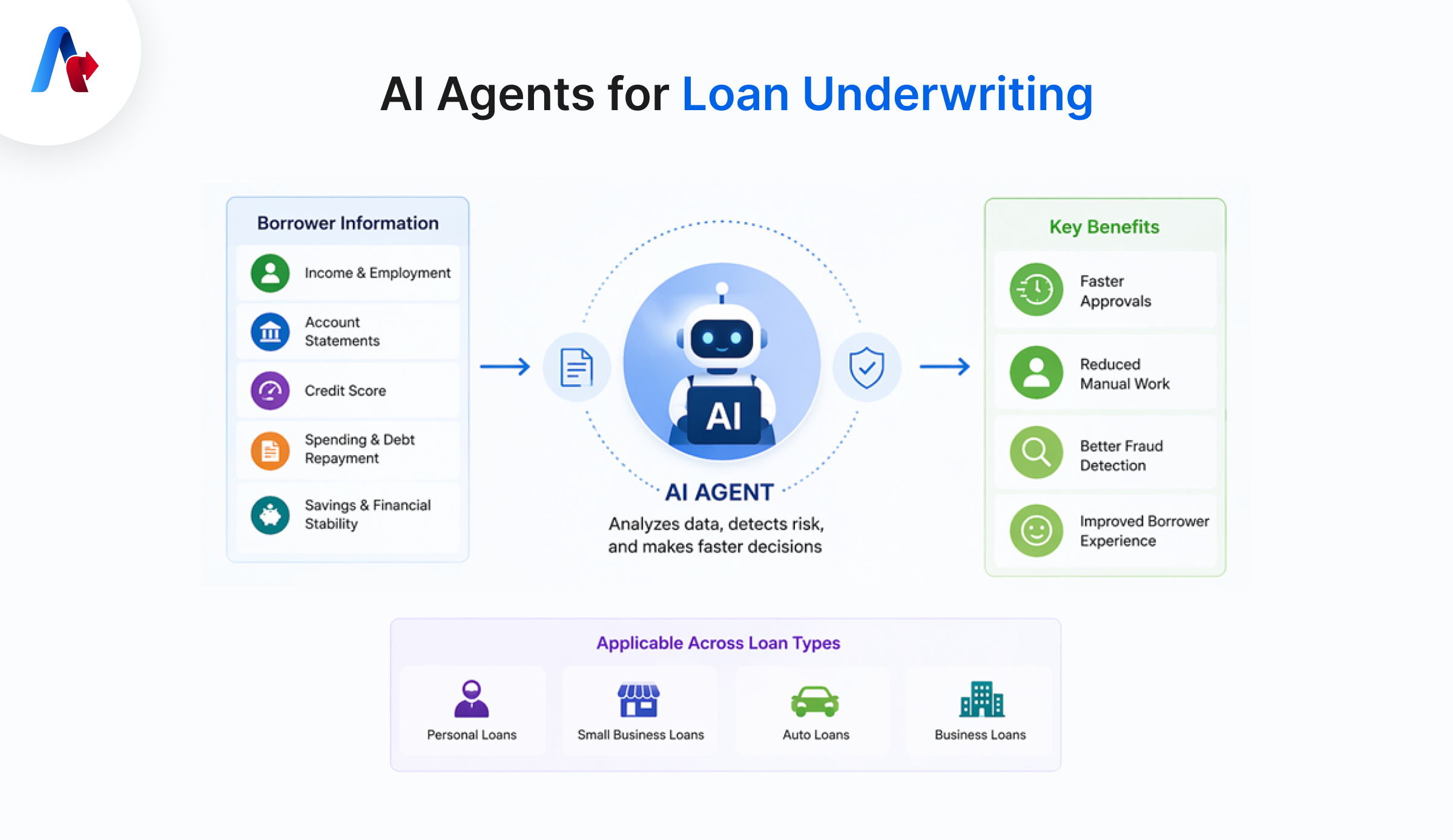

AI agents for loan underwriting can check a borrower's income, employment, account statements, and credit score in less time than a human underwriting team could do it manually. Unlike a simple credit score check, an AI underwriter can look at a borrower's spending, debt levels, repayment behavior, savings, and overall financial stability to determine the risks related to each borrower. This makes it essential in all kinds of loans, from personal loans to small business loans, automobile loans, and business loans.

The most essential advantages of using AI agents for loan underwriting include improved speed, decreased human involvement, enhanced fraud detection ability, and an improved borrower experience. By comparing all kinds of documentation submitted by borrowers, AI agents can spot differences between what is written and other information that is found online.

Mortgage Underwriting with AI Agents: Use Cases & Benefits

Mortgage underwriting automation is more complicated since there is a requirement to include the value of the property, examination of titles, determination of income, and fraud check, among others. This is done through an automatic mortgage underwriting AI agent that would do all these tasks at once by analyzing the borrower data, property data, appraisal, title examination, and lending policies.

This kind of technology will be particularly helpful in-home mortgages, mortgage refinance applications, and cases involving high-value properties where there are many documents that must be examined. For the lenders, it reduces costs. However, for borrowers, it improves the process.

Underwriting Automation Process: Before vs After AI Agents

| Factor | Before AI Agents | After AI Agents |

|---|---|---|

| Document Collection | Underwriters manually gather documents from multiple sources | AI agents automatically extract information from forms, emails, PDFs, and attachments |

| Missing Information | Missing details are identified manually and follow ups take time | Missing information is identified instantly and follow ups are automated |

| Risk Assessment | Risk assessment happens step by step | Risk scoring, fraud detection, and compliance checks happen simultaneously |

| Consistency | Varies by individual and workload | Same logic applied every time |

| Compliance | Compliance reviews are handled separately later in the process | Compliance rules are built directly into the workflow |

| Decision Time | Decisions can take days or weeks | Decisions can be made in hours or minutes |

Top Benefits of Underwriting Automation with AI Agents

The biggest benefits of underwriting automation come from improved speed, productivity, accuracy, and compliance. By manual work and allowing multiple processes to happen at the same time, AI agents help organizations make better decisions faster.

- Faster Decisions - It is no longer a matter of days or weeks but hours or even minutes for applications that earlier required lengthy processing times.

- Lower Costs - Underwriting automation ensures less manual intervention in every case, thus contributing to cost savings.

- Better Accuracy - Since AI-powered agents follow a similar pattern while evaluating each application, the chances of errors are considerably minimized.

- Stronger Compliance - Underwriting AI agents can automatically apply regulatory rules and maintain detailed audit records.

- Improved Employee Experience - Underwriters will now have time to think strategically and deal with complex situations.

Challenges & Risks of Implementing Underwriting AI Agents

The other issue that may affect the deployment of the automated underwriting process is data credibility. Inaccurate or biased information can affect the ability of the system to make reliable risk assessments and decisions. There will also be the challenge of handling huge volumes of structured and unstructured data.

Legacy systems integration may create some difficulties since there will be companies that still use outdated technology. Another problem that may affect the process is compliance as the underwriting agent should be auditable.

Future of Underwriting Automation: Agentic AI Trends for 2026 & Beyond

Underwriting Automation will become more precise in identifying insurance and loan risks while evolving into a more continuous process. While traditionally underwriting involved evaluating a risk at one specific point in time, in the future, organizations are expected to utilize Internet of Things (IoT) data, telemetry, satellite imagery, trends from the market environment, environmental factors, and financial behaviors of individuals to constantly update the assessment of their risk level.

By 2028, 33% of enterprise software applications are expected to include agentic AI, up from less than 1% in 2024. As adoption increases, underwriting AI agents will become more transparent, easier to audit, and more deeply connected to enterprise workflows. Enterprises, to a growing extent, will be needing partners that can help them modernize legacy underwriting processes without interfering with existing operations. This is where Accelirate can help by providing scalable underwriting automation, agentic automation solutions, and intelligent workflow orchestration for insurers, lenders, and financial institutions.

Ready to move from manual underwriting to intelligent automation?

Start with AccelirateFAQs

AI agents help automate underwriting activities such as document authentication, income verification, fraud detection, and regulatory compliance. This enables lenders to make better and quicker judgments with minimal effort.

No. AI agents are only capable of handling repetitive and data-driven activities. Complex transactions need an experienced human to assess and make the final call.

AI underwriting can become regulatory-compliant when the organization builds explainability, transparency, and auditability. The process starts with including regulatory checks at the design stage.

The cost varies based on the scale of the organization, degree of automation, and systems used. Most organizations start with small-scale automation through a pilot program.

In dynamic risk assessment, the risk profile of the client is continually assessed using data obtained regularly. There is no single assessment as in traditional processes.