Quick Summary

With 69% of borrowers uploading documents digitally and 66% preferring online applications, mortgage process automation is moving beyond RPA. AI agents now help lenders read loan-file context, qualify borrowers, clear document gaps, support underwriting readiness, track compliance, and improve broker follow-ups. The right solution should integrate with existing LOS systems, handle complex documents, manage exceptions, support borrower communication, and maintain audit-ready governance.

We all know that RPA has already helped lenders move faster. Today, almost 69% of borrowers upload documents through digital portals, and 66% prefer online applications and e-signing workflows. But a digital submission does not automatically mean a loan file is complete, verified, or ready for underwriting.

That is because the real work begins after the documents are submitted. Teams manually verify them, match them to open conditions, follow up on missing information, and prepare clean files for underwriting, making the process difficult to scale with traditional automation.

That gap between digital submission and manual loan-file review is exactly where AI agents become useful in mortgage automation. Before looking at how they improve the process, let’s first define what mortgage process automation means today.

Want to move loan files faster without replacing your existing systems?

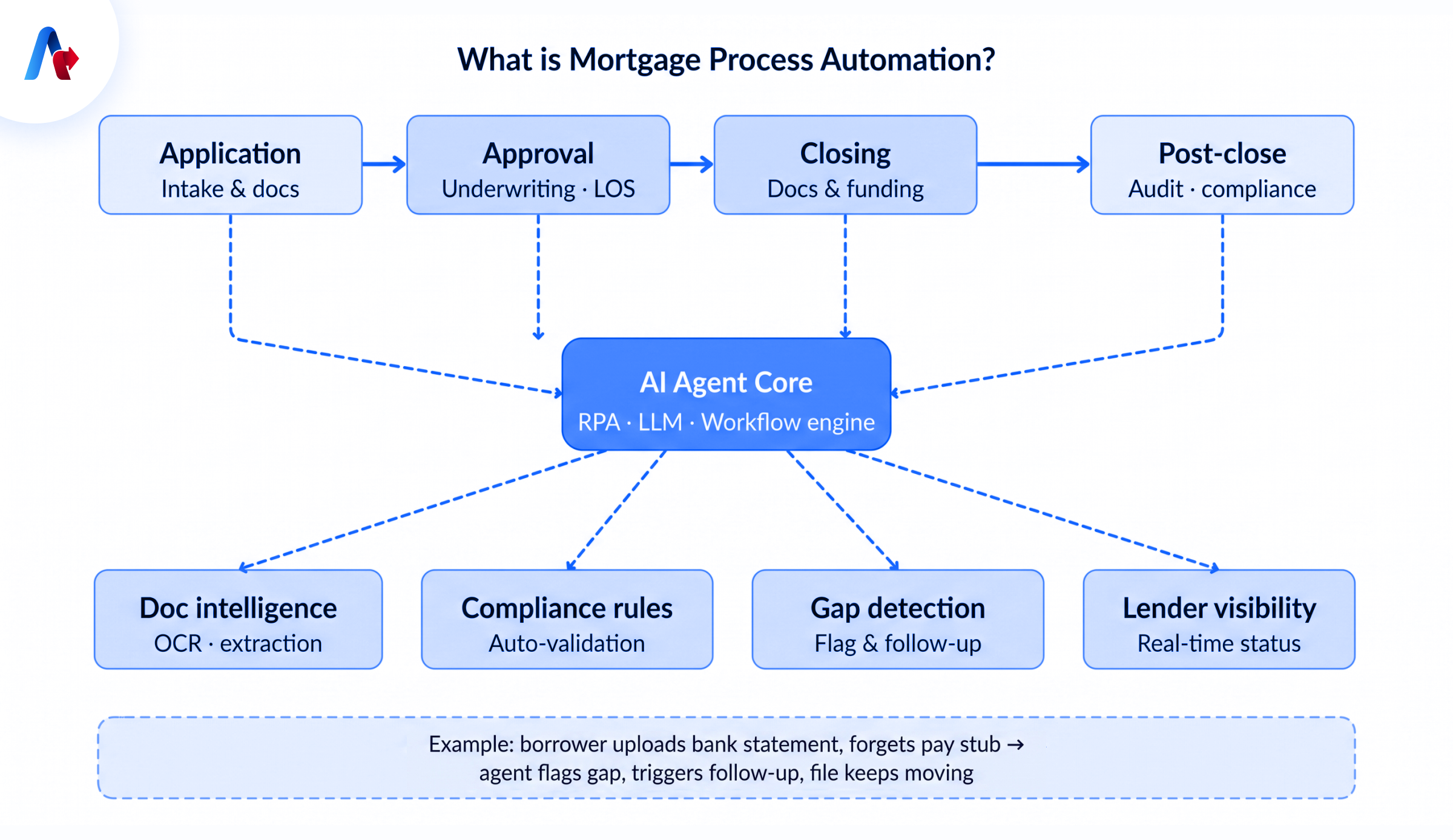

Talk to our expertsWhat is Mortgage Process Automation?

Mortgage process automation uses RPA bots, AI agents, document intelligence, workflow engines, LOS integrations, and compliance rules to streamline work across the mortgage lifecycle. It moves loan files from application to approval, closing, servicing, and post-close review stage with less manual efforts and errors giving lenders better visibility.

The main advantage is that AI agents for mortgage processing close the gap between activity and progress. In traditional systems, documents, emails, conditions, and status updates often sit in different places. AI agents connect that information, show what is missing, and trigger the right follow-up. For example, if a borrower uploads a bank statement but forgets a pay stub, the agent can flag the gap and start the next step before the file stalls.

Where RPA Ends and AI Agents Begin in Mortgage Processing

The major reason lenders are moving from RPA to AI agents is not just because technology is newer. It is because mortgage files now need more checking, follow-up, and review than rule-based automation can handle alone. RPA can move data and send reminders, but it struggles when files have missing documents, unclear emails, or exceptions without any context.

What RPA can and cannot do in mortgage — a clear dividing line

To see the difference clearly, let’s look at where RPA works well in mortgage processing and where it falls short:

| RPA handles | RPA breaks |

|---|---|

| Entering borrower data into the LOS | Non-standard documents like varied pay stubs, tax returns, bank statements, and IDs |

| Updating loan status across systems | Unclear borrower replies across email, portals, chat, or voice |

| Sending basic borrower notifications | Missing or inconsistent information that needs follow-up logic |

| Routing applications between teams | Exception handling across processors, underwriters, and compliance teams |

| Extracting data from structured forms | Connecting income, DTI, repayment history, transaction behavior, and risk signals |

| Logging completed workflow steps | Multi-step underwriting support, fraud review, and compliance-ready decision tracking |

The third generation of mortgage automation — agentic AI

The table clearly shows why the next stage of mortgage automation had to focus on more than workflow speed. That is why mortgage automation has evolved in stages. Gen 1 was OCR and bots, built for data entry, routing, document movement, and status updates. Gen 2 added AI-powered document processing to extract, classify, and validate data from loan documents faster, but it still mainly improved document review.

Now Gen 3 is agentic AI, where mortgage process automation solutions go beyond extraction and start coordinating the next step: identifying what is missing, triggering follow-ups, routing exceptions, supporting underwriting readiness, and helping move the file toward a decision. This helps mortgage teams move from processing files faster to making every file more complete and review ready.

How AI Agents Are Transforming the Mortgage Workflow

Here are a few high-value ways AI agents for mortgage processing are improving day-to-day mortgage workflows:

Borrower qualification and lead triage

AI agents can automate the early stage borrower qualification process by collecting basic borrower details, reviewing credit, bank, payroll, and tax information, and identifying gaps before the file reaches a loan officer. It helps teams qualify mortgage leads faster, spend less time on low-probability applications and route stronger opportunities to loan officers for relationship building and pricing guidance.

Document processing and condition clearing

AI agents can review pay stubs, bank statements, tax returns, IDs, and borrower emails to match received documents against open conditions. The agents can automatically flag issues, update the file, draft the follow-up request, and route only the real exception to the processor. This reduces manual document chasing and speeds up review process.

Underwriting support and compliance readiness

AI agents can help prepare and optimise the loan files by summarizing borrower information, highlighting exceptions, checking policy or compliance gaps, and creating audit-ready records. They do not replace underwriting judgment, but they reduce the time underwriters spend gathering information and give compliance teams better visibility into decision paths, evidence, and review history.

Fraud detection and identity risk flagging

AI agents can also help to check borrower data, identity details, uploaded documents, transaction patterns, and application behavior for fraud signals. If income details, bank activity, documents, or identity information do not align, the agent can flag the risk, create a review trail, and route the case to the right team before the file moves forward.

AI Agents for Mortgage Brokers: Competing at Scale Without Adding Headcount

For mortgage brokers, scale usually breaks in the follow-up layer. A new lead comes in, but then the real work starts: collecting documents, checking what is missing, responding to borrower questions, updating file status, and keeping the loan moving without losing the client’s attention.

AI agents help brokers reduce that coordination load. They can capture borrower intent, collect basic financial details, review incoming documents, flag missing items, draft follow-ups, and show which files need action next. This means brokers spend less time chasing information and more time on the work that actually wins loans: advising borrowers, comparing options, managing pricing, and moving qualified files forward.

In practice, AI agents for mortgage brokers help smaller teams handle more borrower activity without adding headcount at the same pace. The value is not just automation; it is giving every broker a clearer view of which lead is ready, which file is stuck, and what action will move the loan forward.

Turn stalled loan files into decision-ready workflows.

Book a DemoWhat to Look for in a Mortgage Process Automation Solution — and How Accelirate Delivers It

Not all mortgage process automation solutions are built for the way lending teams actually work. The right solution should not only automate tasks, but also improve visibility, reduce exceptions, support compliance, and fit into the systems lenders already use.

5 criteria for evaluating mortgage process automation solutions

- LOS and workflow integration: The solution should be able to connect through APIs or automation layers with existing LOS, document repository, CRM, credit bureau and compliance tools without requiring any platform replacement.

- Mortgage-grade document intelligence: The agent should be able to extract, classify, and validate data from various sources, including unstructured formats and incomplete submissions from pay stubs, tax returns, bank statements, IDs, borrower uploads, and emails.

- Supports exception management: Strong mortgage process automation solutions should help teams identify why a file is stuck, what condition is outstanding, and which next step is needed.

- Improves borrower and team communication: It should help teams send updates, request missing documents, and keep borrowers informed without relying on processors or brokers to chase every item manually.

- Builds in compliance and audit readiness: The agent should log every document check, data validation, exception, workflow step, and human approval with proof for review and audit trails

How Accelirate implements AI agent mortgage automation — the governance-first approach

Accelirate helps lenders automate without disrupting their existing LOS. Rather than replacing core systems or rebuilding workflows from scratch, Accelirate adds intelligence around the steps that slow files down most: document review, missing-information checks, underwriting readiness, borrower follow-ups, and exception routing, all with clear guardrails so teams stay in control.

In mortgage automation, speed only matters if the workflow remains explainable, governed, and auditable. AI agents should help teams move files forward faster, but humans must stay in control of the decisions that carry risk. Namrata Butch - Lead Automation Architect

This governance-first approach makes mortgage process automation safer to scale by keeping human approvals in place, maintaining audit trails, controlling access, improving compliance visibility, and tracking measurable KPIs across the mortgage process.

The Mortgage Teams That Move First Move Fastest

Mortgage process automation is not just about doing the same tasks faster anymore. It is about helping lenders and brokers understand what is slowing each loan down, acting on the right next step, and create cleaner, more decision-ready files. Teams that move first will gain stronger visibility, faster borrower follow-ups, better condition clearing, and more control across the loan lifecycle.

See how Accelirate can help you move beyond RPA with AI agent-driven mortgage process automation. Talk to our experts today!

FAQs

AI agents can assist in automating document review, verification of the borrower, underwriting, fraud detection, and compliance.

AI agents help flagging missing borrower paperwork and trigger the right follow-up faster.

AI agents automate borrower qualification, document processing, condition tracking, underwriting support and triggers follow-ups

You should look for LOS integration, document intelligence, exception handling, borrower communication, and audit trails.